Posted In: Insurance Recovery

Settling with Your Primary Insurer Could Be a Multi-million Dollar Mistake

Settling with Your Primary Insurer Could Be a Multi-million Dollar Mistake

By Caroline L. Marks on July 3, 2014

How the Issue Arises

Assume that a policyholder has CGL coverage from 2006 to 2010. As is typical, it has primary insurance with relatively low limits - $5 million per year - and overlying excess coverage with much greater limits that attach above the $5 million level. Recently, the policyholder has been sued in a high-stakes case seeking many millions in damages over a claim that spans multiple years. As a result of the dispute over coverage, the policyholder settles the underlying case, incurring $20 million in defense and indemnity costs. Thereafter, the primary insurer, which has certain unique coverage defenses available to it, offers to settle the coverage dispute for $4 million. A prompt settlement is attractive to the policyholder, but it will leave the policyholder with significant unreimbursed costs, which it would like to collect from its excess insurers.

Should the Policyholder Settle?

The answer to this question depends on a variety of considerations, but a policyholder needs to understand how settling with its primary insurer for less than the total limits of the primary coverage potentially could reduce or eliminate available excess coverage. This question implicates four cornerstones of the Ohio coverage law system:

Trigger. Under Ohio’s continuous-trigger law, all policies from 2006-2010 are eligible to respond to the underlying claim, because they represent those policies in effect when the alleged continuing bodily injury or property damage took place.

Allocation. Because Ohio has adopted the “all sums” allocation approach, the policyholder is allowed to select the policies from which to receive payment on the claim.

Drop Down Liability. If the full amount of underlying coverage is not available for any reason, the attachment point of the overlying coverage is preserved, and the overlying coverage is not required to “drop down” to pay claims below the bargained-for level.

Contribution. If an insurer is selected by the policyholder and pays a claim on an “all sums” basis, that insurer has certain equitable rights of contribution against other triggered insurers.

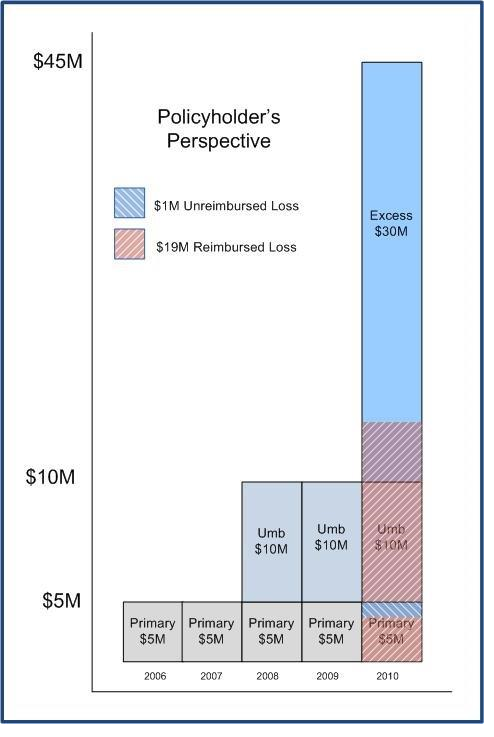

The Policyholder’s Perspective:

Here, the policyholder has $16 million in unreimbursed costs - $20 million minus the $4 million settlement. Under “all sums,” the policyholder selects the 2010 policy year, because that year has the most available coverage. As a result, the policyholder should expect to receive $15 million from its excess insurers:

$ 4 million (paid by primary insurer)

$ 1 million (paid by policyholder)

$ 15 million (paid by excess insurers)

$20 million (total costs)

Applying vertical exhaustion, the umbrella and excess policies will pay $10 million and $5 million respectively. The policyholder will absorb $1 million, which represents the variance between the settlement amount and the full limit of the primary policy, because Ohio law generally does not require excess policies to “drop down.”

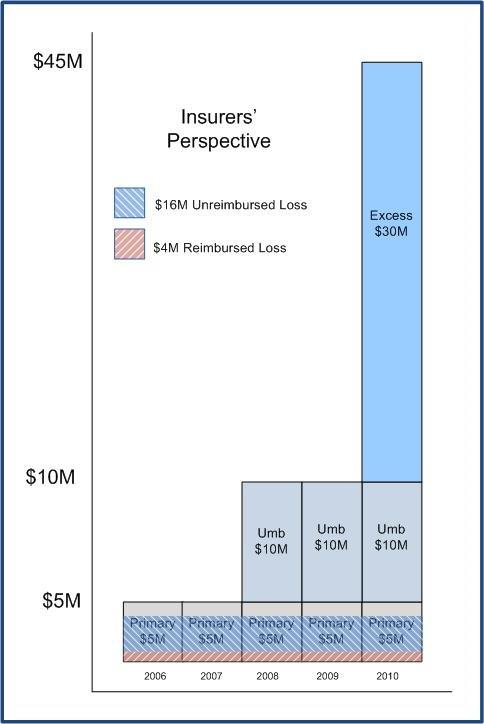

The Insurers’ Perspective:

Everything is the same, except that the insurers assert that by settling with the primary insurer, which had five years of triggered coverage, the policyholder forfeited its right to use “all sums” allocation. According to the insurers, the policyholder now must exhaust the limits of all triggered primary policies before reaching the excess layers. Under this scenario, the policyholder will receive nothing from its excess insurers:

$ 4 million (paid by primary insurer)

$ 16 million (paid by policyholder)

$ 0 million (paid by excess insurers)

$20 million (total costs)

This unfair result should occur, certain insurers would argue, because the combined limits of the triggered primary policies ($25 million) exceed the total costs of the underlying claims. Insurers have had some success with this argument in some jurisdictions, notwithstanding the fact that it creates a strong disincentive to settle, undermines judicial economy, and fails to make a policyholder whole, all in contravention of long-standing Ohio public policy.

Knowledge Is Power.

When faced with the question of whether to settle with a primary insurer, a policyholder would be well-advised to:

Recognize that settling with its primary insurer potentially could reduce or eliminate available excess coverage.

Understand that although Ohio law appears clear, it is not completely settled and that not all states take the same approach. “Choice of law,” referring to which state’s law will apply to a given dispute, can be critical.

Fully analyze the situation and the potential ramifications of any decision before settling with any insurer, including considering the policy language, the magnitude of the claims, and the financial impact of those claims on the policyholder.

Doing these things at the earliest opportunity will give the policyholder important information needed to make an informed decision on the question of whether to risk forfeiting excess coverage by settling with a primary insurer.

This blog is intended to provide information generally and to identify general legal requirements. It is not intended as a form of, or as a substitute for legal advice. Such advice should always come from in-house or retained counsel. Moreover, if this Blog in any way seems to contradict advice of counsel, counsel's opinion should control over anything written herein. No attorney client relationship is created or implied by this Blog. © 2024 Brouse McDowell. All rights reserved.

Share Article Via